Chapter 2: The Arithmetic of Option Premiums

At the time you purchase a particular option, its premium cost

may be $1,000. A month or so later, the same option may be worth

only $800 or $700 or $600. Or it could be worth $1,200 or $1,300

or $1,400. Since an option is something that most people buy with

the intention of eventually liquidating (hopefully at a higher price),

it’s important to have at least a basic understanding of the

major factors which influence the premium for a particular option

at a particular time. There are two, known as intrinsic value and

time value. The premium is the sum of these.

Premium = Intrinsic Value + Time Value

Intrinsic Value

Intrinsic value is the amount of money, if any, that could currently

be realized by exercising the option at its strike price and liquidating

the acquired futures position at the present price of the futures

contract.

At a time when a U.S. Treasury bond futures contract is trading

at a price of 120-00, a call option conveying the right to purchase

the futures contract at a below-the-market strike price of 115-00

would have an intrinsic value of $5,000.

As discussed on page 8, an option that currently has intrinsic

value is said to be "in-the-money" (by the amount of its

intrinsic value). An option that does not currently have intrinsic

value is said to be "out-of-the-money."

At a time when a U.S. Treasury bond futures contract is trading

at 120-00, a calloption with a strike price of 123-00 would be "out-of-the-money"

by $3,000.

Time Value

Options also have time value. In fact, if a given option has no

intrinsic value—because it is currently "out-of-the-money"—its

premium will consist entirely of time value.

What's "Time Value?"

It’s the sum of money option buyers are presently willing

to pay (and option sellers are willing to accept)—over and

above any intrinsic value the option may have—for the specific

rights that a given option conveys. It reflects, in effect, a consensus

opinion as to the likelihood of the option’s increasing in

value prior to its expiration.

The three principal factors that affect an option’s time

value are:

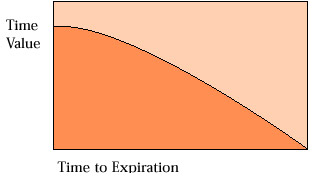

1. Time remaining until expiration. Time value

declines as the option approaches expiration. At expiration, it

will no longer have any time value. (This is why an option is said

to be a wasting asset.)

2. Relationship between the option strike price

and the current price of the underlying futures contract. The further

an option is removed from being worthwhile to exercise—the

further "out-of-the-money" it is—the less time value

it is likely to have.

3. Volatility. The more volatile a market is,

the more likely it is that a price change may eventually make the

option worthwhile to exercise. Thus, the option’s time value

and therefore premium are generally higher in volatile markets.

Past performance is not indicative of future results. Trading futures and options is not suitable for everyone.

There is a substantial risk of loss in trading commodity futures, options and off exchange forex.

|